A SWOT analysis for Open Banking

Strengths, Weaknesses, Opportunities and Threats of Open Banking

What is SWOT Analysis?

A SWOT analysis is basically an output of a brainstorming session and identifying and analyzing an organization or an individual project. A SWOT analysis is an incredibly simple, yet powerful tool to help you develop your business strategy.

What is Open Banking?

Open banking is the practice of sharing financial information electronically, securely, and only with the approval of customer using APIs. This has been a trending topic in the financial industry for some time now. The APIs allow TPPs to access financial information efficiently, which promotes the development of new apps and services. If you are new to Open Banking, have a look at my previous article which explains the basics of Open Banking.

Now, let’s conduct a SWOT analysis for Open Banking and identify the Strengths, Weaknesses, Opportunities, and Threats!

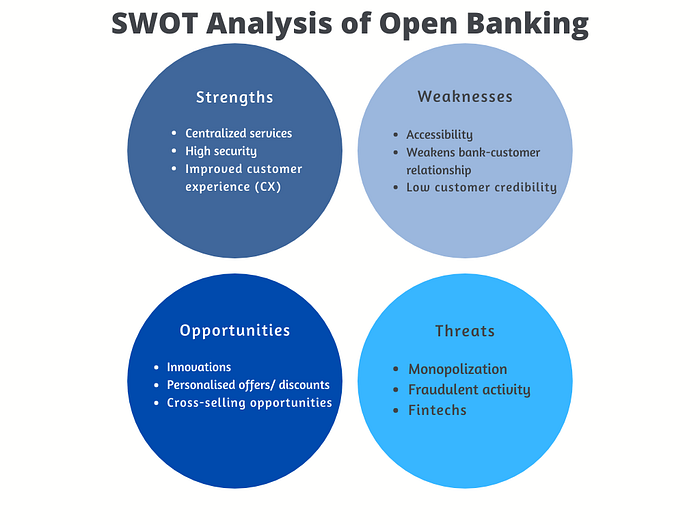

Strengths

- Centralized services: Open Banking provides banks with full control over the various services the customers need: advice, loans, transfers, and financing into a single dashboard. Customers who maintain their accounts in multiple banks can use a single TPP to access all their accounts and initiate payments without the need to login via different security protocols.

- High security: Open Banking mandates that these Open APIs that expose confidential data to meet several security requirements. Open Banking Security Profile and Financial-grade API (FAPI) that uses OAuth 2.0 and OpenID Connect (OIDC) which are already established in the security domain are some of the measures taken to increase the security of APIs and customer data.

- Improved customer experience (CX): Several Open Banking specifications (the Open Banking Standard, Consumer Data Standards CX standards and guidelines) have come up with their own customer experience guidelines. These guidelines the customers gain a seamless and frictionless experience with their bank regardless of the TPP application they choose.

Weaknesses

- Accessibility: The digitization Open Banking brings in to the banking experience is more likely to be adopted by the Millenials than the Baby Boomers. In addition to that, the fact that open banking requires regular internet access is not in a position to benefit certain users who do not have access to the internet.

- Weakens bank-customer relationship: Because everything is handled digitally, the face-to-face encounters between the customer and the bank are getting smaller. This can lead to a breakdown in the relationship.

- Low customer credibility: Customers lack a considerable amount of credibility towards Open Banking. It is partly due to the fear of sharing their data, as well as to their lack of knowledge of how it works. Customers fear to make a change in their financial authority and payment behaviour due to this concern.

Opportunities

- Innovations: Open Banking introduces new roles and stakeholders to the typical banking ecosystem. Banks can make the most of these roles (For example, AISP, PISP in PSD2) and can create new products and services. The TPPs can come up with new propositions and business models while offering great customer experiences.

For example, online payments to an e-merchant, on behalf of a customer, creating an alternative to card payments for both customers and merchants. - Personalised offers and discounts: With open banking and open APIs, stakeholders can obtain more insight into financial data. This is advantageous in several financial analysis which will eventually generate more opportunities for the banking customers. For example, wealth planning and insurance schemes, personalized offers and loyalty rewards, financial management and education.

- Cross-selling opportunities: Open API standards compel financial institutions to share mandatory data for free. However, the banks can charge a fee for the additional data they can share, with the consumer’s consent. This can lead to generating revenue rather than maintaining a conventional core banking system.

Threats

- Monopolization: Banking today mostly comprises of one/few major banks that define the market dynamics. Open banking has been introduced to make banking a more competitive business. One of its main goals is to offer a shared chance of success for all financial service providers. Even shifting to open banking can still result in the same monopoly these huge banks maintain and it’s an apparent threat in the financial industry.

- Fraudulent activity: The financial institutions sharing customer data even with extreme security means is a potential gold mine for fraudsters, particularly through identity fraud. Fear not, Strong Customer Authentication, Transaction Risk Analysis and Fraud Rules are already available. (These are some of the features supported by WSO2 Open Banking, which is a great way to comply with your Open Banking requirements. To know more about WSO2 Open Banking, see https://wso2.com/solutions/financial/open-banking/).

- Fintechs: The growth of those companies that have replaced the banks is a major drawback for Open Banking. The Fintech market is growing. Their services are diverse and more and more there are a large number of them in all countries.

Conclusion

Open Banking comes to the market with its own advantages and disadvantages. We can categories these to Strengths, Weaknesses, Opportunities and Threats. There’s no doubt that Open Banking brings more to the table than being regulatory compliance. The Strengths and Opportunities it of Open Banking is undoubtedly changing the market dynamics and eventually result in better innovations and better customer experience. Additionally, these Weaknesses and Threats are already tackled by several Open Banking solutions in the industry. Embrace the new changes to keep up the pace in banking — one of the fastest-moving industries.